Search

Search our 7.940 News Items

CATEGORIES

We found 19 books in our category 'TAXES'

We found 19 news items

We found 19 books

Tielt

Kritak/Lannoo

2020

condition: As new/comme neuf/wie neu/als nieuw.

book number: 202205282347

Achter de schermen van de BBI. De memoires van een caractériel

Pb, in-8, 280 pp.

De langverwachte memoires van Karel Anthonissen (°1954) over de mankementen van onze fiscus. Er loopt heel wat grondig mis met onze belastinginning. Er zitten zo veel mazen in het net dat de fiscus een pak minder ophaalt dan waar de staat recht op heeft. Dat is een van de redenen waarom de overheid moet lenen en waarom we een grote staatsschuld hebben. Wat het nog erger maakt, is dat de belastingontwijking heel ongelijk verdeeld is. In de praktijk geldt het omgekeerde van de officiële filosofie van ons belastingstelsel: de sterkste schouders torsen de kleinste last.

De langverwachte memoires van Karel Anthonissen (°1954) over de mankementen van onze fiscus. Er loopt heel wat grondig mis met onze belastinginning. Er zitten zo veel mazen in het net dat de fiscus een pak minder ophaalt dan waar de staat recht op heeft. Dat is een van de redenen waarom de overheid moet lenen en waarom we een grote staatsschuld hebben. Wat het nog erger maakt, is dat de belastingontwijking heel ongelijk verdeeld is. In de praktijk geldt het omgekeerde van de officiële filosofie van ons belastingstelsel: de sterkste schouders torsen de kleinste last.

ANTHONISSEN Karel@ wikipedia

€ 20.0

Paris

Fayard

1972

FRA

condition: Very good/Très bel état/Sehr gut/Zeer goed

book number: 202302270340

Histoire de l'impôt Livre II: Du XVIIIe au XXIe siècle

Hardcover, relié, jq, in-8, 870 pp., notes bibliographiques, bibliographie, index. Collection 'Les Grandes Etudes Historiques'.

Hardcover, relié, jq, in-8, 870 pp., notes bibliographiques, bibliographie, index. Collection 'Les Grandes Etudes Historiques'.Qu'on se souvienne des efforts accomplis par un Richelieu, un Pierre le Grand, en Russie, et bien d'autres, pour construire des Etats modernes sur des sociétés agraires inaptes à subir leurs prélèvements.

L'histoire de l'impôt est donc celle des sociétés, vue au travers de ce qui leur a permis de s'affranchir du régime du pillage comme du système hiérarchisé de prestations de biens et de services, pour arriver à la lente construction des Etats actuels.

En montrant dans cet ouvrage l'incidence constante de l'impôt sur les événements politiques et économiques, l'auteur projette un éclairage nouveau sur bien des problèmes qui sont aujourd'hui d'une actualité brûlante.

L'auteur:

Inspecteur général des Finances, ancien commissaire général à la Productivité, docteur ès lettres, Gabriel Ardant a toujours considéré que l'expérience professionnelle devait éclairer la science et l'histoire, et réciproquement. Tous ses ouvrages tels " Technique de l'Etat ", " Le Monde en friche " s'insèrent dans cette ligne.

ARDANT Gabriel@ wikipedia

€ 150.0

Bruxelles/Brussel

Pro Civitate

1966

BEL

condition: Very good

book number: 19640042

l'Impôt dans le cadre de la ville et de l'état. De belasting in het raam van stad en staat. Colloque international / Internationaal colloquium Spa 6-9-IX-1964. Actes / Handelingen

Broché 340 pp. Pro civitate. Collection Histoire/Historische uitgaven, in 8to, n. 13, 1966. Supplément: page des errata.

ARNOULD Maurice-A., e.a.@ wikipedia

€ 40.0

Brussel

Fiscale Hogeschool

1993

BEL

condition: Very good/Très bel état/Sehr gut/Zeer goed

book number: 202110120225

Liber amicorum Maeckelbergh: fiscaliteit op de vooravond van de XXIste eeuw.

Paperback, grote in-8, pp., illustraties, bibliografische noten, bibliografie, index/register, met de nominatieve lijst van de 826 voorintekenaars.

Niet zomaar een boek over belastingen.

Niet zomaar een boek over belastingen.

AUTENNE Jacques, TIBERGHIEN A., e.a.@ wikipedia

€ 30.0

Paris

Charles Hingray

1839

FRA

condition: Quelques rousseurs dans le texte. Very fine set, firmly bound.

book number: 18390001

Traité des droits d'enregistrement, de timbre, d'hypothèques et des contraventions à la loi du 25 ventôse an XI - Tômes I à V

Halfleather. Titre doré sur le dos. Deuxième édition. Tôme I = 615 pp. Tôme II = 664 pp. Tôme III = 816 pp. Tôme IV = 1.068 pp. Tôme V (qui date de 1841) = 230 pp. + Dictionnaire de l'enregistrement de 680 pp. au moyen duquel on retrouve facilement toutes les lois, décrets, avis du conseil d'état, décisions, judiciaire ou administratives, et questions que contient le traité. Soit au total 4.073 pages. Poids/weight: 4.260 grams. Note: 25 ventôse an XI = 16 mars 1803.

CHAMPIONNIERE M. & RIGAUD M. @ wikipedia

€ 200.0

Brussel

Moniteur

1937

BEL

condition: Couverture défraichie. Bon à l'intérieur

book number: 19370033

Rapport sur la simplification des lois d'impôts. Verslag over de vereenvoudiging der belastingswetten.

Softcover, 4to, 184 pp. De auteur was Hoogleraar aan de Universiteit Leuven en Koninklijk Commissaris voor de Fiscale Vereenvoudiging.

COART-FRESART Paul@ wikipedia

€ 20.0

Leuven

ACCO

2004

INT

condition: Very good/Très bel état/Sehr gut/Zeer goed

book number: 201807131240

Mooie meisjes betalen geen belastingen. Een kritiek op het sociaal-democratische paradigma.

Gesigneerd door de auteur. Pb, in-8, 124 pp. Bevat na elk hoofdstuk een handige samenvatting met stellingnamen. Op p. 63 voorspelt De Neve terroristische aanslagen en een migratiestroom vanuit Afrika.

DE NEVE Luc@ wikipedia

€ 15.0

Zutphen/Deventer

de Walburg Pers/Kluwer

1982

BEL

condition: Very good

book number: 19820105

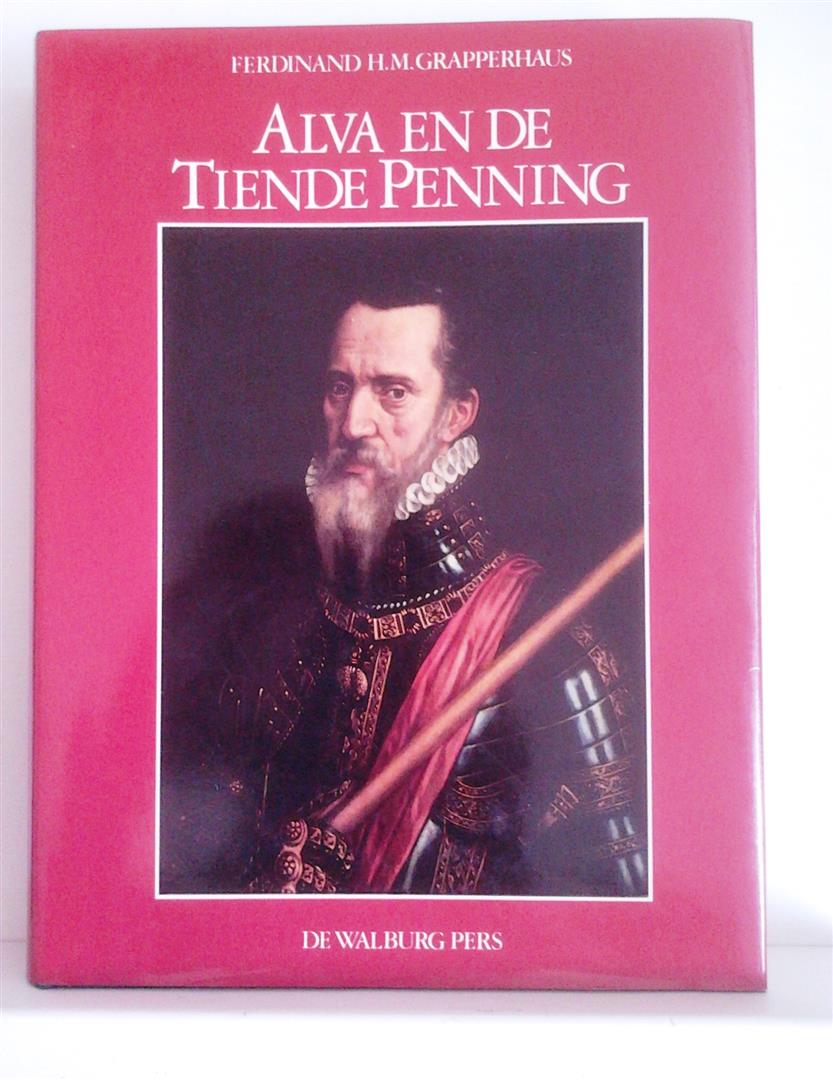

Alva en de Tiende Penning.

Hardcover, blauw linnen met zilveropdruk, geïllustreerde stofwikkel (portret van Alva uit 1568 door Willem Key), 399 pp., illustraties in ZW, kaartje van de Nederlanden in 1559, bibliografie, index. Diepgaande studie over de belastinghervorming in onze gewesten. Tiende penning = 10% belasting. Hoe belastingen van invloed waren (geen oorzaak van) op de opstand tegen Spanje. De auteur onderscheidt 6 periodes in de langdurige pogingen om tot een belastinghervorming te komen en om meer eenheid in de Nederlanden te vestigen onder het koninklijk gezag. Uiteindelijk wordt de tiende penning in 1572 op de lange baan geschoven en in 1574 afgeschaft. Op p. 119 vindt men een interessante verdeling van de waarde van de geproduceerde goederen in 1570. Daaruit blijkt de dominantie van Brabant en Vlaanderen. Op p. 263 de integrale tekst van het Geuzenlied. Over hoe belastingen aangewend kunnen worden om te onderdrukken of om het volk te dienen. Ook over onderhandelde, genegocieerde belastingen en het botsen van belangen.

GRAPPERHAUS Ferdinand H.M.@ wikipedia

€ 50.0

Zutphen-Deventer

Meijburg & Co

1989

INT

condition: Very good/Très bel état/Sehr gut/Zeer goed

book number: 19890149

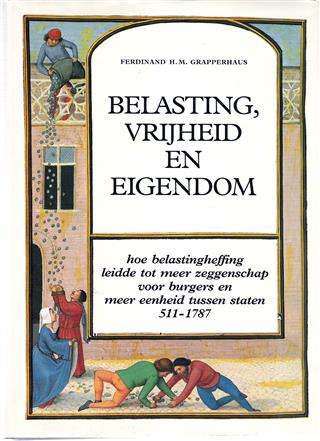

Belasting, vrijheid en eigendom. Hoe belastingheffing leidde tot meer zeggenschap voor burgers en meer eenheid tussen staten 511-1787.

Hardcover with ill. dj., 4to., 407 pp. Illustraties en gravures in ZW en kleur. Zeer uitgebreide bibliografie. De basisvraag van dit boek: hoe beïnvloedt belastinginning de staatkundige emancipatie in West-Europa en Noord-Amerika. De auteur komt tot het besluit dat de vrijwillige instemming van burgers om tot belastingheffing over te gaan hen inspraak gaf in het staatkundig bestel. De uniformisering van de belasting leidt dan tot natievorming.

GRAPPERHAUS,F.H.M.@ wikipedia

€ 30.0

Brussel

EHSAL Fiscale Hogeschool

1990

BEL

condition: Very good/Très bel état/Sehr gut/Zeer goed. De reproductie van een historisch 'Placcaet' van 40x50 cm op artisanaal papier ontbreekt.

book number: 201905201817

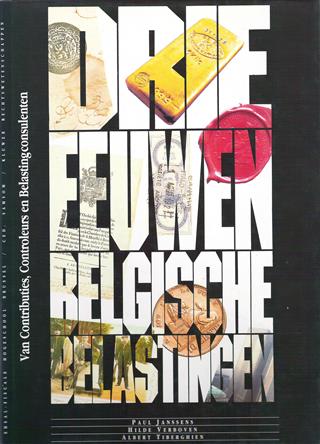

Drie Eeuwen Belgische Belastingen - Van contributies controleurs en belastingconsulenten.

GENUMMERDE BIBLIOFIELE EDITIE: nr 97/150. GESIGNEERD DOOR DE 3 AUTEURS EN DOOR WILLY MAECKELBERGH. Hardcover, gebonden in zwart kunstlederen band met goudopdruk, geïllustreerde stofwikkel, 4to, 432 pp., 350 ZW en kleurillustraties, bibliografie, Summary in English, (Handbook on the history of three centuries Belgian taxation). Zeldzaam. TOEGEVOEGD: ERRATA OP 1 PAGINA A4. Noot LT: nooit werd het verhaal van de belastingen zo boeiend in woord en beeld gebracht. Referentiewerk van topniveau dat ons steeds doet beseffen dat zonder belastingen een Staat niet bestaat.

GENUMMERDE BIBLIOFIELE EDITIE: nr 97/150. GESIGNEERD DOOR DE 3 AUTEURS EN DOOR WILLY MAECKELBERGH. Hardcover, gebonden in zwart kunstlederen band met goudopdruk, geïllustreerde stofwikkel, 4to, 432 pp., 350 ZW en kleurillustraties, bibliografie, Summary in English, (Handbook on the history of three centuries Belgian taxation). Zeldzaam. TOEGEVOEGD: ERRATA OP 1 PAGINA A4. Noot LT: nooit werd het verhaal van de belastingen zo boeiend in woord en beeld gebracht. Referentiewerk van topniveau dat ons steeds doet beseffen dat zonder belastingen een Staat niet bestaat.Pro memorie: Onmiddellijk na de bezetting van de Oostenrijkse Nederlanden door de Franse revolutionairen worden in 1794 de fiscale vrijdommen afgeschaft: "AVERTISSEMENT; Le Magistrat de Bruxelles avertit le public, qu'il a donné les ordres le plus positifs à la Trésorerie de cette ville (Bruxelles, LT), de ne plus permettre qu'aucun habitant puisse jouir de l'exemption d'aucun impôt, sous quelque prétexte que se puisse être. s. J.F. DE MENDIVIL." (zie p. 153)

Op p. 38 vindt men de informatieve kaart van 'De Belgische Provincies en de Zuidnederlandse Vorstendommen uit de 18de eeuw' van de hand van Marie-Rose Thielemans. De opsomming daaronder is onmisbaar voor een begrip van de complexiteit van het 'Belgische' terrein tijdens het Ancien Régime.

Dat 'terrein' bestond uit volgende entiteiten:

•vorstendom of prinsbisdom Luik

•graafschap Namen

•hertogdom Brabant

•graafschap Henegouwen

•graafschap Vlaanderen

•heerlijkheid Mechelen

•hertogdom Luxemburg

•hertogdom Bouillon

•het Doornikse

•Frans-Vlaanderen

•Landen van Overmaas (graafschap Dalhem)

•vorstendom Stavelot-Malmédy

•hertogdom Limburg

Op pp. 44 e.v. vindt men een gedegen uitleg over de Provinciale Staten en hun inspraak in de fiscaliteit.

Op p. 88 een kaart van de Belgische Départements onder het Franse Bewind (1795-1815).

JANSSENS Paul Prof. Dr - VERBOVEN Hilde Drs - TIBERGHIEN Albert Prof Dr@ wikipedia

€ 200.0

Leuven

ACCO

2006

BEL

condition: Very good/Très bel état/Sehr gut/Zeer goed

book number: 202404090320

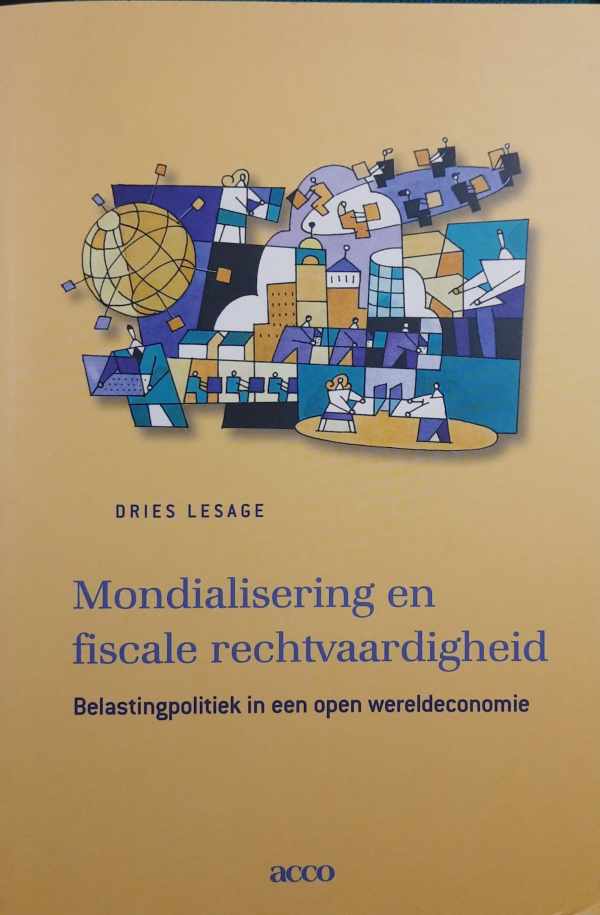

Mondialisering en fiscale rechtvaardigheid - Belastingpolitiek in een open wereldeconomie

1ste druk. Paperback, in-8, 377 pp., tabellen, bibliografische noten, bibliografie.

Op welk niveau wordt er nu eigenlijk beslist over belastingen en over een vermogensbelasting in het bijzonder? In de coulissen van de macht, stupid.

Op welk niveau wordt er nu eigenlijk beslist over belastingen en over een vermogensbelasting in het bijzonder? In de coulissen van de macht, stupid.

LESAGE Dries@ wikipedia

€ 25.0

Gent

borgerhoff & lamberigts

2012

BEL

condition: Very good/Très bel état/Sehr gut/Zeer goed

book number: 201810261730

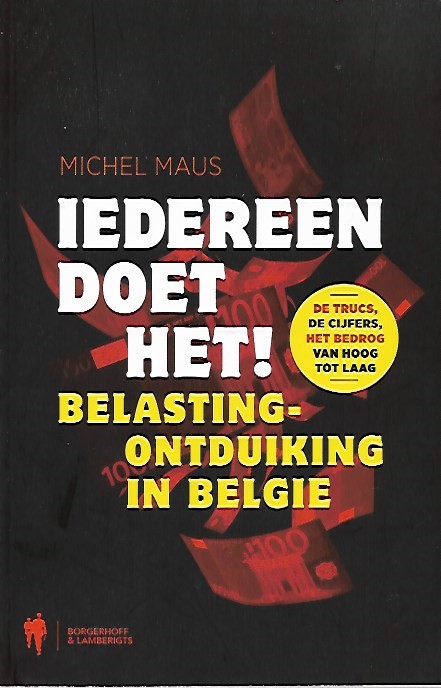

Iedereen doet het ! Belastingontduiking in België. De trucs, de cijfers, het bedrog van hoog tot laag.

Tweede druk. Pb, in-8, 231 pp.

In 2010 vertegenwoordigde de zwarte economie 17,9 procent van het Belgische BBP. (studie van Friedrich Schneider) (p. 96)

Kritiek: 1) In zijn historisch overzicht (hfst 5) slaat Michel Maus de Franse Revolutie over. Wil dit nu net de periode zijn die leidde tot een zeer grote ongelijkheid in de (onroerende) vermogens of - beter - de vermogens aan de top van de piramide verplaatste.

2) Het boek bevat geen voet- of eindnoten en er is ook geen bibliografie aanwezig. Daardoor blijft het ondermaats.

3) Er wordt te weinig beklemtoond dat de overheid zelf de belastingontduiking 'stuurt' in deze of gene richting en dat de groten vaak de dans ontspringen omdat zij de fiscale spitstechnologie kunnen betalen.

In 2010 vertegenwoordigde de zwarte economie 17,9 procent van het Belgische BBP. (studie van Friedrich Schneider) (p. 96)

Kritiek: 1) In zijn historisch overzicht (hfst 5) slaat Michel Maus de Franse Revolutie over. Wil dit nu net de periode zijn die leidde tot een zeer grote ongelijkheid in de (onroerende) vermogens of - beter - de vermogens aan de top van de piramide verplaatste.

2) Het boek bevat geen voet- of eindnoten en er is ook geen bibliografie aanwezig. Daardoor blijft het ondermaats.

3) Er wordt te weinig beklemtoond dat de overheid zelf de belastingontduiking 'stuurt' in deze of gene richting en dat de groten vaak de dans ontspringen omdat zij de fiscale spitstechnologie kunnen betalen.

MAUS Michel@ wikipedia

€ 15.0

Brugge

die Keure

2015

BEL

condition: As new/comme neuf/wie neu/als nieuw.

book number: 202106170944

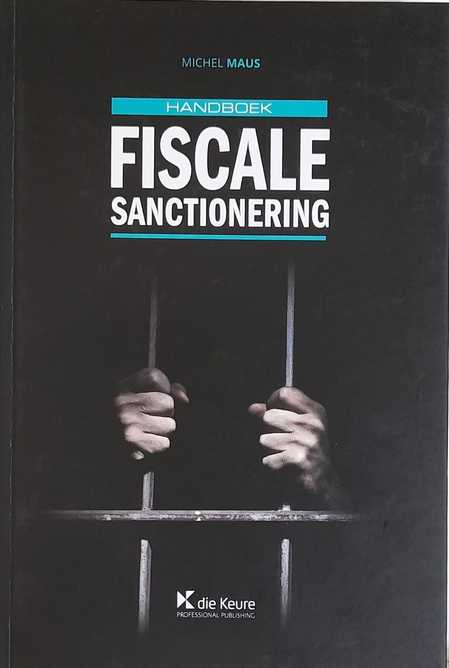

Handboek fiscale sanctionering

Hardcover, in-8, 300 pp., bibliografische noten.

Behandelt zowel de federale als de gewestelijke materie.

Een geheel hoofdstuk is gewijd aan het 'onrechtmatig verkregen bewijs', een heikele materie.

Maar is Maus niet de vos die de passie preekt?

Behandelt zowel de federale als de gewestelijke materie.

Een geheel hoofdstuk is gewijd aan het 'onrechtmatig verkregen bewijs', een heikele materie.

Maar is Maus niet de vos die de passie preekt?

MAUS Michel@ wikipedia

€ 40.0

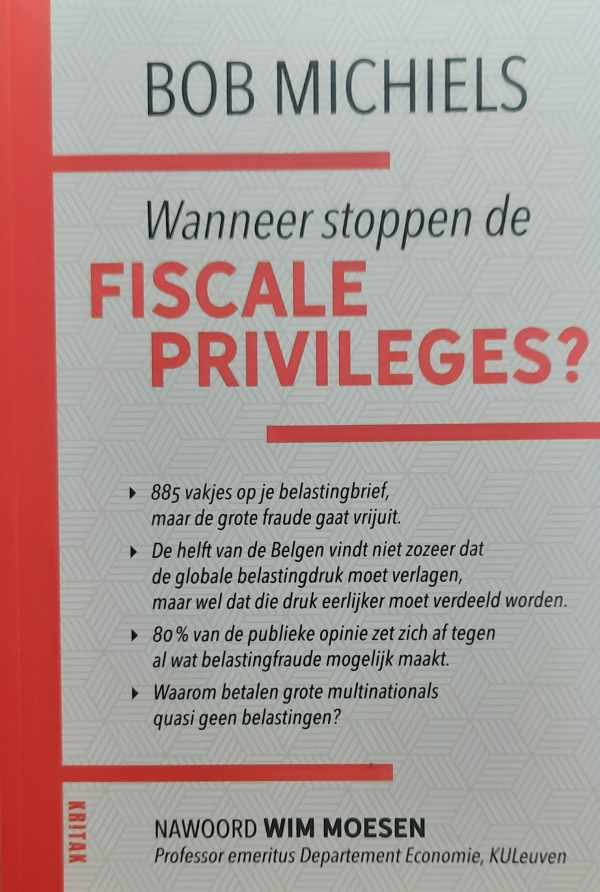

Wanneer stoppen de fiscale priveleges?

Paperback, in-8, 222 pp., bibliografische noten.- Twee op de drie Belgen vinden het huidige belastingsysteem onrechtvaardig. - De helft van de Belgen vindt niet zozeer dat de globale belastingdruk moet verlagen, maar wel dat die druk eerlijker moet verdeeld worden.

- 80% van de publieke opinie zet zich af tegen al wat belastingfraude mogelijk maakt.

- De sociale ongelijkheid en de armoede worden door de coronapandemie nog verder uitgediept, waardoor het noodzakelijk wordt dat iedereen - dus ook de rijksten - financieel bijdragen. Het is totaal abject dat ons huidig belastingbeleid grote multinationals van belastingen vrijstelt, waardoor miljarden voor de samenleving verdwijnen, die vervolgens via bezuinigingen in de gezondheidszorg, de uitkeringen, de cultuur en het onderwijs moeten worden gerecupereerd.

- Een vermogenskadaster is niet alleen technisch haalbaar, het zou zelfs op enkele maanden een feit kunnen zijn. Alleen de politieke wil ontbreekt.

- Wat is het belang van LuxLeaks, SwissLeaks, BahamaLeaks, de Panama Papers, de Paradise Papers? De bekendste topeconomen pleiten ervoor om de rijken opnieuw te gaan belasten op basis van hogere tarieven voor de hoogste schijven, zoals in de gouden jaren '50-'60 van de vorige eeuw toegepast, zonder de economische hoogconjunctuur in gevaar te brengen.

Nawoord van Wim Moesen, Professor emeritus Departement Economie, KU Leuven.

Bron: Flaptekst, uitgeversinformatie.

Noot LT: Dat de uitgever zo'n verhelderend boek uitgeeft zonder namenregister mag een beroepsfout en luiheid worden genoemd. Foei, Lannoo/Kritak. Daarom hebben we de moeite genomen om zelf een vereenvoudigd register aan te maken: Fernand Huts, Alexia Bertrand, Emmanuel Levinas, John Stuart Mill, Thomas Piketty, Adam Smith, Noreena Hertz, Leonardo Boff, Shell, Apple, Walmart, Hobbes, Paul Verhaeghe, Mark Elchardus, Branko Milanovic, Donald Trump, Frank Vandenbroucke, Erik Schokkaert, Koen Raes, Marc Coucke, Charles Michel, Johan Van Overtveldt, CMA-Medina, Gino Deraedt, Frederica Verheyden, Sacha Dierckx, Oxfam, Klaus Schwab, World Economic Forum, Bert Bultick, Knack, Theo Franken, Bart De Wever, Ingrid Robeyns, Bill Gates, Jeff Bezos, Marc De Vos, Joseph Stiglitz, Isha Ambani, Anand Piramal, Hillary Clinton, John Kerry, Beyoncé, Sarah Kuypers, Ive Marx, Jos Geysels, Erik Vlaminck, Apache, Crédit Suisse, Matthias Somers, Minerva, Marc Reynebeau, Egbert Reynebeau, Margrethe Vestager, Tim Cook, Steve Jobs, Laurene Powell Jobs, Forbes, Emiel Dullaert, MacKenzie Scott, Gabriel Zucman, Ingrid Robeyns, The Guardian, Elon Musk, SpaceX, Joe Biden, Marco Van Hees, Van Peteghem, ICIJ, Maagdeneilanden, Mauritius, Bahama's, Bermuda, Cyprus, Nederland, Luxemburg, Starbucks, Google, Amazon, Apple, Dexia, Fortis, Ikea, GAFA, PriceWaterhouseCoopers, Jean-Claude Juncker, Lars Bové, Disney, Kaaimaneilanden, Wedco, Jan Van de Poel, EURODAD, Christian Aid, OESO, Common Consolidated Corporate Tax Base, Europese Raad, EURACTIV, David Bowie, Joan Collins, John Malkovich, Michael Schumacher, Paul Bocuse, Marokko, Bahrein, Saudi-Arabië, Baby Doc Duvalier, Haïti, HSBC, Michel Claise, Mossack Fonseca, Moebarak, Juan Carlos, Xi Jinping, Poetin, Pedro Almodovar, Dominique Strauss-Kahn, Lionel Messi, Michel Platini, Franco Dragone, de Spoelberch, UBS, Société Générale, Royal Bank of Canada, KBC, Bank Degroof, Pierre Moscovici, Michel Maus, BBI, Kristof Calvo, PVDA, PTB, Peter Vanvelthoven, Facebook, Nike, Madonna, Bono, Jared Kushner, Justin Trudeau, Queen Elisabeth II, Trouw, Tim Cook, Wouter Lips, Jersey-route, Jan Tuerlinckx, Michel Maus, Gibraltar, Louise Hoon, Janet Yellen, IMF, Internationaal Monetair Fonds, China, India, Alex Cobham, Didier Reynders, de Mévius, Van Damme, Frère, Huts, Colruyt, De Nul, Ackermans & van Haaren, Singapore, Fernand Huts, Kent, Guernsey, Mont Saint Michel Trust, Zonamerica Ltd, Uruguay, Montevideo, Phoebus Foundation, Jan Jambon, Liechtenstein, Peter Bernaerts, Bernard Arnault, Louis Vuitton Foundation, Saatchi Gallery, Robrecht Vanderbeeken, ACOD, Carlos Slim, John Crombez, Elio Di Rupo, Peter Mertens, BEL20, Jan Rosier, Eurostat, François-Xavier de Donnea, Stefaan Van Hecke, Jean Gol, Bernard Clerfayt, Frank Philipsen, Dirk Van der Maelen, Herman Van Rompuy, Armand De Decker, Chodiev, Tractebel, Walter De Smedt, Yves Liégeois, Omega Diamonds, Peter Van Calster, Karel Anthonissen, Fincel Files, Belfius, BNP Paribas Fortis, Lesbos, Ronald Commers, Rik Pinxten, Sacha Dierckx, John Maynard Keynes, Boël, AB Inbev, Vlerick, Bosteels, Bostoen, Delhaize, Lhoist, Berghmans, d'Ieteren, Van Hove, Alexander De Croo, Koen Geens, Boelwerf, Karel De Gucht, Luc Van der Kelen, Ludo Cornelis, Eric Goeman, NV Ranson-Cannière, Pieter Timmermans, Isabel Albers, Bilderberg, Pascal Saint-Amans, Herman Matthijs, Leonce Eraly, Theo Klingels, Financieel Actie Netwerk, Rekenhof, Marc Leemans, VOKA, Bruno Peeters, Dries Lesage, Anton Delbarre, Comeos, Vitor Gaspar, Paul Krugman, Barack Obama, Liliane Bettencourt, l'Oréal, Paul De Grauwe, Anthony Atkinson, John Vandaele, Sarah Kuypers, Bruno Blondé, Wouter Ryckbosch (123), Vincent Van Quickenborne, Luc Coene, Anton Delbare, Ultimate Beneficial Owne (UBO), Sacha Dierckx, Gwendolyn Rutten, Bart Van Craeynest, Macron, Joël De Ceulaer, Franklin Roosevelt, Chantal Mouffe, Aristoteles, Mark Delanote, lvan Van de Cloot, Kantar, Paul Magnette, Carl Devos, Georges-Louis Bouchez, Bart Sturtewagen, Denis-Emmanuel Philippe, Assuralia, Dirk Verhofstadt, Liberales, Herman De Croo, Bart Somers, Karl Popper, Andreas Tirez, John Rawls, Ronald Dworkin, Ewald Pironet, Nicolas Bouteca, Mathias De Clercq, ram Wauters, Servais Verherstraeten, Joris Vandenbroucke, Thomas Dermine, Michaël Van Droogenbroeck, Kathleen Van Brempt, Frank Parkin, Daan Isebaert, Zakia Khattabi, Petra De Sutter, Bart Staes, BASF, Zara, Massimo Dutti, Pull & Bear, Wouter Beke, Peter De Roover, Edmund Burke, Herman De Bode, Thomas Nys, Bart Eeckhout, Pierre Wunsch, Eric Van den Broele, Graydon, Jan Denys, David Hope, Julian Limberg, Kevin Spiritus, Koen Schoors, Vincent Stuer, Thijs Delrue, Hans Vanaken, Club Brugge, Leen Dierick, Cercle Brugge, Jupiler Pro Ligue, Simon Mignolet, Ignace Vandewalle, Football Leaks, Thibaut Courtois, Sophie Wilmès, Erik Buyst (218).

Omdat we belastingen een vervelende materie vinden, laten we het aan de superrijken over om ze niet te betalen.

MICHIELS Bob, MOESEN Wim prof dr em (nawoord)@ wikipedia

€ 27.5

Amsterdam/Antwerpen

Contact

2013

NLD

condition: Very good

book number: 201504110120

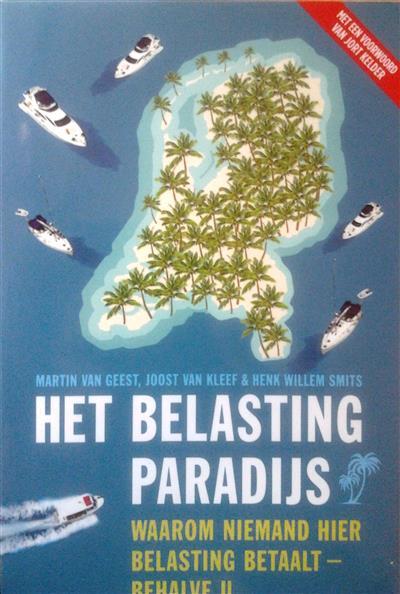

het belastingparadijs - waarom niemand hier belasting betaalt - behalve u

3de druk. Pb, in-8, 256 pp., index

VAN GEEST Martin, VAN KLEEF Joost, SMITS Henk Willem@ wikipedia

€ 15.0

Berchem

EPO

2013

BEL

condition: Very good/Très bel état/Sehr gut/Zeer goed

book number: 202001242210

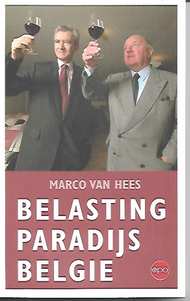

Belastingparadijs België (vertaling van Les riches aussi ont le droit de payer des impôts -2013)

Paperback, in-8, 180 pp., geen illustraties, enkele tabellen, bibliografische noten.De tabel op pp. 22-23 is cruciaal en geeft de lijst van de 50 multinationale bedrijven die in 2011 konden genieten van in totaal bijna 17 miljard euro belastingverminderingen. Op een winst van 52,5 miljard euro vóór belastingen betaalden ze nauwelijks 0,9 miljard of 1,78 % belastingen.

Een stuitende vaststelling die aangeeft wie voor financieminister Didier Reynders belangrijk is: diegenen die rijk zijn hebben er alle belang bij hem in het zadel te houden.

Marco Van Hees is belastinginspecteur bij het Ministerie van Financiën.

VAN HEES Marco@ wikipedia

€ 50.0

Bruxelles

CRISP

2023

BEL

condition: Nieuw/Neuf/New/Neu

book number: 202312030022

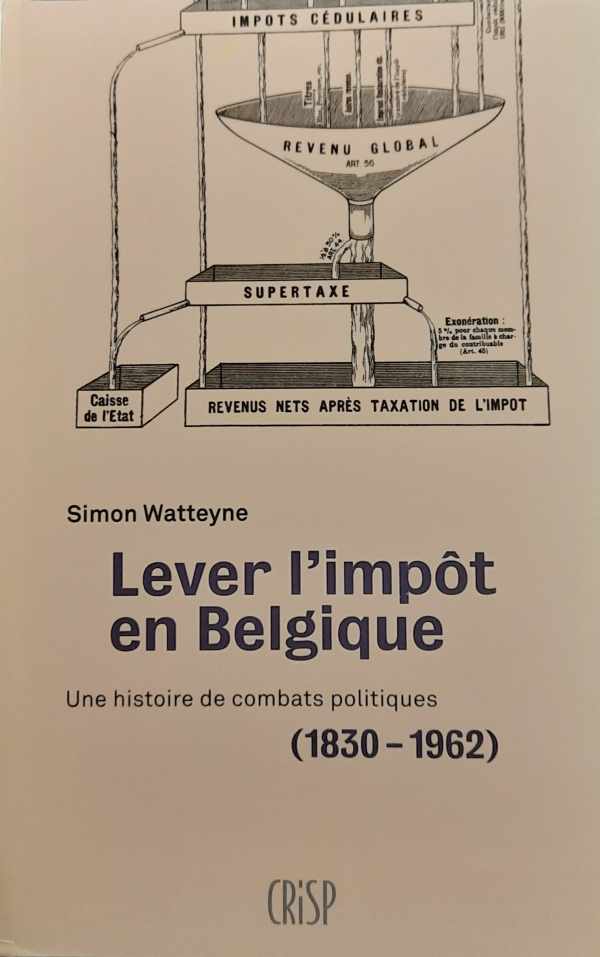

Lever l'impôt en Belgique. Une histoire de combats politiques (1830-1962)

Broché, in-8, 422 pp., graphiques, notes bibliographiques, bibliographie.

Le désintérêt de la population pour le dossier fiscal est choquant. Toutefois, la politique fiscale d’un pays constitue la pierre angulaire de la démocratie.

Le désintérêt de la population pour le dossier fiscal est choquant. Toutefois, la politique fiscale d’un pays constitue la pierre angulaire de la démocratie.

WATTEYNE Simon@ wikipedia

€ 35.0

New York

Simon and Schuster

1986

INT

condition: A few markings otherwise clean.

book number: 202303021136

A history of taxation and expenditure in the Western world

Thick paperback, large in-8, 734 pp., bibliographical notes, impressive bibliography. Reference work.

In this comprehensive analysis of social systems of taxation and budgeting, the authors provide detailed examples from ancient Mesopotamia and Egypt, Greece and Rome, the Middle Ages in Europe, and modern times to show how governments through the ages have raised money and spent it. They examine the two essential activities of government - taxing and spending - against the background of the societies in which they were imbedded and the development of government's administrative capacities. They also argue that government mobilization of resources involves critical human concerns waging war and providing for the welfare of the people.

About the Authors

Carolyn Webber is an associate specialist at the Institute of Urban and Regional Development at the University of California, Berkeley. She has also been an associate specialist with the Graduate School of Public Policy at Berkeley.

Aaron Wildavsky is a professor of political science and public policy at the University of California, Berkeley. He has also been president of the Russell Sage Foundation and dean of the Graduate School of Public Policy at Berkeley. His many books include The Politics of the Budgetary Process, Presidential Elections (with Nelson W. Polsby), Speaking Truth to Power, and How to Limit Government Spending.

In this comprehensive analysis of social systems of taxation and budgeting, the authors provide detailed examples from ancient Mesopotamia and Egypt, Greece and Rome, the Middle Ages in Europe, and modern times to show how governments through the ages have raised money and spent it. They examine the two essential activities of government - taxing and spending - against the background of the societies in which they were imbedded and the development of government's administrative capacities. They also argue that government mobilization of resources involves critical human concerns waging war and providing for the welfare of the people.

About the Authors

Carolyn Webber is an associate specialist at the Institute of Urban and Regional Development at the University of California, Berkeley. She has also been an associate specialist with the Graduate School of Public Policy at Berkeley.

Aaron Wildavsky is a professor of political science and public policy at the University of California, Berkeley. He has also been president of the Russell Sage Foundation and dean of the Graduate School of Public Policy at Berkeley. His many books include The Politics of the Budgetary Process, Presidential Elections (with Nelson W. Polsby), Speaking Truth to Power, and How to Limit Government Spending.

WEBBER Carolyn, WILDAVSKY Aaron @ wikipedia

€ 60.0

New Haven/London

Yale University Press

1972

FRA

condition: No dj. Very good

book number: 19720121

The Fiscal System in Renaissance France

Hardcover, in-8, 385 pp., bibliography, index. Note LT: Wolfe argues that there was 'discontinuity, i.e. a set of institutions and attitudes so different from those of a prior period'. This view on history was new in 1972. Contract of Poissy (21/10/1561) (p. 123-124); Forced alienations of church property (p. 126-129); Venality: the worst expedient (p. 129-132). Well written and important work. Explains how taxes and royal government (i.e. the power to tax) were interwoven and what was the role of the church in all this. Quote: "There is an intriguing similarity between the demands raised at Pontoise (1561) to strip the church of part of its wealth and the debates of 1789 that led to the famous assignats." (p. 122)

WOLFE Martin@ wikipedia

€ 75.0

We found 19 news items

“Here’s the deal: If you spent $3 on your coffee this morning, that’s more than what 55 major corporations paid in taxes in recent years.”

ID: 202110200288

Land: USA

Klokkenluider die LuxLeaks op gang bracht verliest zijn zaak voor het beroepshof

ID: 202105191122

Corporate tax dodging continues to make headlines and feature prominently in policy discussions around the world. But disclosing exactly how companies secretly skirt taxes remains a risky act.

Europe’s top human rights court upheld the conviction of whistleblower Raphaël Halet, a former PwC employee who downloaded tax records from a work computer that became a key part of Lux Leaks. The 2014 ICIJ investigation revealed how nearly 340 global firms slashed their tax bills by making confidential deals with the Luxembourg government. The exposé sparked momentum across Europe to end industrial-scale tax dodging.

The court ruled in favor of Luxembourg and PwC, an accounting giant that designed complex financial structures and helped clients cut deals uncovered in Lux Leaks — allowing some of the world’s largest companies to pay less than 1% tax.

But the decision was made with some strong opposition. Two judges penned a dissent stating that the ruling created an impossibly high bar for future whistleblowers to meet, stressing the importance of repeated leaks to reinforce public awareness around corporate tax dodging.

The ruling came out the same week that the European Union General Court ruled in favor of Amazon and Luxembourg in a case challenging another sweetheart tax deal — a setback in the European Commission's campaign to force Amazon to repay about $300 million in taxes.

Europe’s top human rights court upheld the conviction of whistleblower Raphaël Halet, a former PwC employee who downloaded tax records from a work computer that became a key part of Lux Leaks. The 2014 ICIJ investigation revealed how nearly 340 global firms slashed their tax bills by making confidential deals with the Luxembourg government. The exposé sparked momentum across Europe to end industrial-scale tax dodging.

The court ruled in favor of Luxembourg and PwC, an accounting giant that designed complex financial structures and helped clients cut deals uncovered in Lux Leaks — allowing some of the world’s largest companies to pay less than 1% tax.

But the decision was made with some strong opposition. Two judges penned a dissent stating that the ruling created an impossibly high bar for future whistleblowers to meet, stressing the importance of repeated leaks to reinforce public awareness around corporate tax dodging.

The ruling came out the same week that the European Union General Court ruled in favor of Amazon and Luxembourg in a case challenging another sweetheart tax deal — a setback in the European Commission's campaign to force Amazon to repay about $300 million in taxes.

Land: LUX

Categorie: BUSINESS - GESJOEMEL

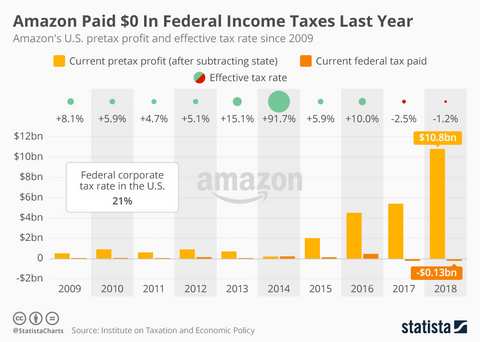

Gigant Amazon betaalt voor tweede jaar op rij geen belastingen !

ID: 201902200418

Despite doubling its profits, Amazon has paid zero dollars in federal taxes for the second successive year. A recent report from the Institute on Taxation and Economic Policy (ITEP) has raised huge questions about the tax-paying habits of the tech giant.

Land: USA

Billionaire fortunes grew by $2.5 billion a day last year as poorest saw their wealth fall

ID: 201901212004

Published: 21 January 2019

Billionaire fortunes increased by 12 percent last year – or $2.5 billion a day - while the 3.8 billion people who make up the poorest half of humanity saw their wealth decline by 11 percent, reveals a new report from Oxfam today. The report is being launched as political and business leaders gather for the World Economic Forum in Davos, Switzerland.

‘Public Good or Private Wealth’ shows the growing gap between rich and poor is undermining the fight against poverty, damaging our economies and fuelling public anger across the globe. It reveals how governments are exacerbating inequality by underfunding public services, such as healthcare and education, on the one hand, while under taxing corporations and the wealthy, and failing to clamp down on tax dodging, on the other. It also finds that women and girls are hardest hit by rising economic inequality.

Winnie Byanyima, Executive Director of Oxfam International, said:

“The size of your bank account should not dictate how many years your children spend in school, or how long you live – yet this is the reality in too many countries across the globe. While corporations and the super-rich enjoy low tax bills, millions of girls are denied a decent education and women are dying for lack of maternity care.”

The report reveals that the number of billionaires has almost doubled since the financial crisis, with a new billionaire created every two days between 2017 and 2018, yet wealthy individuals and corporations are paying lower rates of tax than they have in decades.

Getting the richest one percent to pay just 0.5 percent extra tax on their wealth could raise more money than it would cost to educate the 262 million children out of school and provide healthcare that would save the lives of 3.3 million people.

Just four cents in every dollar of tax revenue collected globally came from taxes on wealth such as inheritance or property in 2015. These types of tax have been reduced or eliminated in many rich countries and are barely implemented in the developing world.

Tax rates for wealthy individuals and corporations have also been cut dramatically. For example, the top rate of personal income tax in rich countries fell from 62 percent in 1970 to just 38 percent in 2013. The average rate in poor countries is just 28 percent.

In some countries, such as Brazil, the poorest 10 percent of society are now paying a higher proportion of their incomes in tax than the richest 10 percent.

At the same time, public services are suffering from chronic underfunding or being outsourced to private companies that exclude the poorest people. In many countries a decent education or quality healthcare has become a luxury only the rich can afford. Every day 10,000 people die because they lack access to affordable healthcare. In developing countries, a child from a poor family is twice as likely to die before the age of five than a child from a rich family. In countries like Kenya a child from a rich family will spend twice as long in education as one from a poor family.

Cutting taxes on wealth predominantly benefits men who own 50 percent more wealth than women globally, and control over 86 percent of corporations. Conversely, when public services are neglected poor women and girls suffer most. Girls are pulled out of school first when the money isn’t available to pay fees, and women clock up hours of unpaid work looking after sick relatives when healthcare systems fail. Oxfam estimates that if all the unpaid care work carried out by women across the globe was done by a single company it would have an annual turnover of $10 trillion – 43 times that of Apple, the world’s biggest company.

“People across the globe are angry and frustrated. Governments must now deliver real change by ensuring corporations and wealthy individuals pay their fair share of tax and investing this money in free healthcare and education that meets the needs of everyone - including women and girls whose needs are so often overlooked. Governments can build a brighter future for everyone – not just a privileged few,” added Byanyima.

Billionaire fortunes increased by 12 percent last year – or $2.5 billion a day - while the 3.8 billion people who make up the poorest half of humanity saw their wealth decline by 11 percent, reveals a new report from Oxfam today. The report is being launched as political and business leaders gather for the World Economic Forum in Davos, Switzerland.

‘Public Good or Private Wealth’ shows the growing gap between rich and poor is undermining the fight against poverty, damaging our economies and fuelling public anger across the globe. It reveals how governments are exacerbating inequality by underfunding public services, such as healthcare and education, on the one hand, while under taxing corporations and the wealthy, and failing to clamp down on tax dodging, on the other. It also finds that women and girls are hardest hit by rising economic inequality.

Winnie Byanyima, Executive Director of Oxfam International, said:

“The size of your bank account should not dictate how many years your children spend in school, or how long you live – yet this is the reality in too many countries across the globe. While corporations and the super-rich enjoy low tax bills, millions of girls are denied a decent education and women are dying for lack of maternity care.”

The report reveals that the number of billionaires has almost doubled since the financial crisis, with a new billionaire created every two days between 2017 and 2018, yet wealthy individuals and corporations are paying lower rates of tax than they have in decades.

Getting the richest one percent to pay just 0.5 percent extra tax on their wealth could raise more money than it would cost to educate the 262 million children out of school and provide healthcare that would save the lives of 3.3 million people.

Just four cents in every dollar of tax revenue collected globally came from taxes on wealth such as inheritance or property in 2015. These types of tax have been reduced or eliminated in many rich countries and are barely implemented in the developing world.

Tax rates for wealthy individuals and corporations have also been cut dramatically. For example, the top rate of personal income tax in rich countries fell from 62 percent in 1970 to just 38 percent in 2013. The average rate in poor countries is just 28 percent.

In some countries, such as Brazil, the poorest 10 percent of society are now paying a higher proportion of their incomes in tax than the richest 10 percent.

At the same time, public services are suffering from chronic underfunding or being outsourced to private companies that exclude the poorest people. In many countries a decent education or quality healthcare has become a luxury only the rich can afford. Every day 10,000 people die because they lack access to affordable healthcare. In developing countries, a child from a poor family is twice as likely to die before the age of five than a child from a rich family. In countries like Kenya a child from a rich family will spend twice as long in education as one from a poor family.

Cutting taxes on wealth predominantly benefits men who own 50 percent more wealth than women globally, and control over 86 percent of corporations. Conversely, when public services are neglected poor women and girls suffer most. Girls are pulled out of school first when the money isn’t available to pay fees, and women clock up hours of unpaid work looking after sick relatives when healthcare systems fail. Oxfam estimates that if all the unpaid care work carried out by women across the globe was done by a single company it would have an annual turnover of $10 trillion – 43 times that of Apple, the world’s biggest company.

“People across the globe are angry and frustrated. Governments must now deliver real change by ensuring corporations and wealthy individuals pay their fair share of tax and investing this money in free healthcare and education that meets the needs of everyone - including women and girls whose needs are so often overlooked. Governments can build a brighter future for everyone – not just a privileged few,” added Byanyima.

Afghanistan: opiumproductie stijgt fors

ID: 201711230605

Afghan opium production has jumped to record levels this year. According to the latest "Afghanistan Opium Survey" released jointly by the Afghan Ministry of Counter Narcotics and United Nations Office on Drugs and Crime (UNODC), overall production rose by 87 percent compared to last year, to 9,000 metric tons. This is partly due to a 63 percent increase in poppy cultivated cropland, to 328,000 hectares in 2017. Also, the yield has increased by 15 percent to around 27 kilos of opium per hectare.

Afghanistan is the world's top cultivator of poppy from which opium and heroin are produced. The cultivation and sale is a source of revenue for the Taliban insurgency and other terrorist groups, as they levy taxes from farmers cultivating the crop. At the beginning of this week, the U.S. Air Force bombed production facilities in the south Afghan province of Helmand, which is the most prolific production area within Afghanistan.

The steep rise in production also means that more cheap but high quality heroin will be available on illicit markets across the world.

on the consumption side: overdoses rise in the USA

Pro memorie: Op 11 november 2017 bracht de VRT in het journaal een propaganda-reportage: de boeren in Afghanistan waren begonnen met het planten en oogsten van saffraan ... op 3.000 hectaren. Hoe goedgelovig kan je zijn? Met geen woord werd gerept over de enorme productiestijging in de opium-business.

Land: AFG

LUXLEAKS WHISTLEBLOWERS THANKED AS TAX PROBES CONTINUE

ID: 201601130925

ICIJ, 20160113

Belgium has been ordered to recover $765 million in unpaid taxes from 35 multinational corporations after the European Commission said tax breaks granted to the companies were illegal.

The ruling was the latest in a series of investigations, led by European Union competition commissioner Margrethe Vestager, into special tax concessions offered by European countries to lure the business of multinational corporations.

Last year the commission made similar rulings against Luxembourg and the Netherlands concerning their tax deals with Fiat and Starbucks respectively. Investigations into Ireland’s tax arrangements with Apple and Luxembourg’s agreement with Amazon are ongoing.

The commission has not named the 35 companies affected by the Belgium ruling, but brewer ABInBev (which produces Budweiser, Stella Artois and other popular brands of beer) and BP are reported to be among them.

ICIJ’s Luxemourg Leaks investigation, published in 2014, revealed the inner workings of many of these types of secret arrangements that some of the world’s biggest companies make with government authorities in order to slash their tax bills.

On the same day the commission’s latest ruling was announced, an interview with commissioner Vestager was published by EurActiv in which she denounced Luxembourg’s decision to prosecute two whistleblowers and a journalist in relation to leaked tax documents.

“LuxLeaks could not have happened if it was not for the whistleblower and the team of investigative journalists. The two worked very well together to change the momentum of the debate about corporate taxation in Europe,” Vestager said.

“I think everyone should thank both the whistleblower and the investigative journalists who put a lot of work into this.”

The trial of whistleblower and former PricewaterhouseCoopers employee Antoine Deltour, another unnamed whistleblower, and journalist and ICIJ member Edouard Perrin is set to begin in Luxembourg on April 26.

Belgium has been ordered to recover $765 million in unpaid taxes from 35 multinational corporations after the European Commission said tax breaks granted to the companies were illegal.

The ruling was the latest in a series of investigations, led by European Union competition commissioner Margrethe Vestager, into special tax concessions offered by European countries to lure the business of multinational corporations.

Last year the commission made similar rulings against Luxembourg and the Netherlands concerning their tax deals with Fiat and Starbucks respectively. Investigations into Ireland’s tax arrangements with Apple and Luxembourg’s agreement with Amazon are ongoing.

The commission has not named the 35 companies affected by the Belgium ruling, but brewer ABInBev (which produces Budweiser, Stella Artois and other popular brands of beer) and BP are reported to be among them.

ICIJ’s Luxemourg Leaks investigation, published in 2014, revealed the inner workings of many of these types of secret arrangements that some of the world’s biggest companies make with government authorities in order to slash their tax bills.

On the same day the commission’s latest ruling was announced, an interview with commissioner Vestager was published by EurActiv in which she denounced Luxembourg’s decision to prosecute two whistleblowers and a journalist in relation to leaked tax documents.

“LuxLeaks could not have happened if it was not for the whistleblower and the team of investigative journalists. The two worked very well together to change the momentum of the debate about corporate taxation in Europe,” Vestager said.

“I think everyone should thank both the whistleblower and the investigative journalists who put a lot of work into this.”

The trial of whistleblower and former PricewaterhouseCoopers employee Antoine Deltour, another unnamed whistleblower, and journalist and ICIJ member Edouard Perrin is set to begin in Luxembourg on April 26.

State of the Union 2015: Let's turn the page and fight inequality.

ID: 201501210958

(extract)

President Obama's State of the Union address as prepared for delivery on Jan. 20, 2015:

Mr. Speaker, Mr. Vice President, Members of Congress, my fellow Americans:

(...)

Now, the truth is, when it comes to issues like infrastructure and basic research, I know there's bipartisan support in this chamber. Members of both parties have told me so. Where we too often run onto the rocks is how to pay for these investments. As Americans, we don't mind paying our fair share of taxes, as long as everybody else does, too. But for far too long, lobbyists have rigged the tax code with loopholes that let some corporations pay nothing while others pay full freight. They've riddled it with giveaways the superrich don't need, denying a break to middle class families who do.

This year, we have an opportunity to change that. Let's close loopholes so we stop rewarding companies that keep profits abroad, and reward those that invest in America. Let's use those savings to rebuild our infrastructure and make it more attractive for companies to bring jobs home. Let's simplify the system and let a small business owner file based on her actual bank statement, instead of the number of accountants she can afford. And let's close the loopholes that lead to inequality by allowing the top one percent to avoid paying taxes on their accumulated wealth. We can use that money to help more families pay for childcare and send their kids to college. We need a tax code that truly helps working Americans trying to get a leg up in the new economy, and we can achieve that together.

President Obama's State of the Union address as prepared for delivery on Jan. 20, 2015:

Mr. Speaker, Mr. Vice President, Members of Congress, my fellow Americans:

(...)

Now, the truth is, when it comes to issues like infrastructure and basic research, I know there's bipartisan support in this chamber. Members of both parties have told me so. Where we too often run onto the rocks is how to pay for these investments. As Americans, we don't mind paying our fair share of taxes, as long as everybody else does, too. But for far too long, lobbyists have rigged the tax code with loopholes that let some corporations pay nothing while others pay full freight. They've riddled it with giveaways the superrich don't need, denying a break to middle class families who do.

This year, we have an opportunity to change that. Let's close loopholes so we stop rewarding companies that keep profits abroad, and reward those that invest in America. Let's use those savings to rebuild our infrastructure and make it more attractive for companies to bring jobs home. Let's simplify the system and let a small business owner file based on her actual bank statement, instead of the number of accountants she can afford. And let's close the loopholes that lead to inequality by allowing the top one percent to avoid paying taxes on their accumulated wealth. We can use that money to help more families pay for childcare and send their kids to college. We need a tax code that truly helps working Americans trying to get a leg up in the new economy, and we can achieve that together.

Land: USA

IMF on tax shift in Belgium

ID: 201412162207

Tax policy. The tax policy measures of the government program contain a net reduction in labor taxes and a useful simplification of various social security abatement schemes, which should help limit unwanted distortions. At the same time we see scope for going further in tax reform. Income from capital is not taxed uniformly, and a more harmonized treatment would put the taxation of such income on a more equal footing with labor income. Property taxes could be rebalanced from transaction taxes to recurrent taxes on immovable property. This would stabilize tax collection and enhance labor mobility. We also see scope for reducing deviations from the standard VAT rate, e.g., for electricity, and to increase environmental taxes. Revenue gains from such reforms would be available to reduce labor taxes further.

Read more ...

Read more ...

OECD SOCIAL, EMPLOYMENT AND MIGRATION WORKING PAPERS No. 163 - TRENDS IN INCOME INEQUALITY AND ITS IMPACT ON ECONOMIC GROWTH

ID: 201412090905

20141209 - ABSTRACT

1. In most OECD countries, the gap between rich and poor is at its highest level since 30 years.

Today, the richest 10 per cent of the population in the OECD area earn 9.5 times the income of the poorest

10 per cent; in the 1980s this ratio stood at 7:1 and has been rising continuously ever since. However, the

rise in overall income inequality is not (only) about surging top income shares: often, incomes at the

bottom grew much slower during the prosperous years and fell during downturns, putting relative (and in

some countries, absolute) income poverty on the radar of policy concerns. This paper explores whether

such developments may have an impact on economic performance.

2. Drawing on harmonised data covering the OECD countries over the past 30 years, the

econometric analysis suggests that income inequality has a negative and statistically significant impact on

subsequent growth. In particular, what matters most is the gap between low income households and the rest

of the population. In contrast, no evidence is found that those with high incomes pulling away from the rest

of the population harms growth. The paper also evaluates the “human capital accumulation theory” finding

evidence for human capital as a channel through which inequality may affect growth. Analysis based on

micro data from the Adult Skills Survey (PIAAC) shows that increased income disparities depress skills

development among individuals with poorer parental education background, both in terms of the quantity

of education attained (e.g. years of schooling), and in terms of its quality (i.e. skill proficiency).

Educational outcomes of individuals from richer backgrounds, however, are not affected by inequality.

3. It follows that policies to reduce income inequalities should not only be pursued to improve

social outcomes but also to sustain long-term growth. Redistribution policies via taxes and transfers are a

key tool to ensure the benefits of growth are more broadly distributed and the results suggest they need not

be expected to undermine growth. But it is also important to promote equality of opportunity in access to

and quality of education. This implies a focus on families with children and youths – as this is when

decisions about human capital accumulation are made -- promoting employment for disadvantaged groups

through active labour market policies, childcare supports and in-work benefits.

Note LT: the famous book of Piketty (Capital) is not mentioned in the bibliography of this report!; Methodology: measurement of inequality with the use of Gini.

Read the report in PDF here ...

1. In most OECD countries, the gap between rich and poor is at its highest level since 30 years.

Today, the richest 10 per cent of the population in the OECD area earn 9.5 times the income of the poorest

10 per cent; in the 1980s this ratio stood at 7:1 and has been rising continuously ever since. However, the

rise in overall income inequality is not (only) about surging top income shares: often, incomes at the

bottom grew much slower during the prosperous years and fell during downturns, putting relative (and in

some countries, absolute) income poverty on the radar of policy concerns. This paper explores whether

such developments may have an impact on economic performance.

2. Drawing on harmonised data covering the OECD countries over the past 30 years, the

econometric analysis suggests that income inequality has a negative and statistically significant impact on

subsequent growth. In particular, what matters most is the gap between low income households and the rest

of the population. In contrast, no evidence is found that those with high incomes pulling away from the rest

of the population harms growth. The paper also evaluates the “human capital accumulation theory” finding

evidence for human capital as a channel through which inequality may affect growth. Analysis based on

micro data from the Adult Skills Survey (PIAAC) shows that increased income disparities depress skills

development among individuals with poorer parental education background, both in terms of the quantity

of education attained (e.g. years of schooling), and in terms of its quality (i.e. skill proficiency).

Educational outcomes of individuals from richer backgrounds, however, are not affected by inequality.

3. It follows that policies to reduce income inequalities should not only be pursued to improve

social outcomes but also to sustain long-term growth. Redistribution policies via taxes and transfers are a

key tool to ensure the benefits of growth are more broadly distributed and the results suggest they need not

be expected to undermine growth. But it is also important to promote equality of opportunity in access to

and quality of education. This implies a focus on families with children and youths – as this is when

decisions about human capital accumulation are made -- promoting employment for disadvantaged groups

through active labour market policies, childcare supports and in-work benefits.

Note LT: the famous book of Piketty (Capital) is not mentioned in the bibliography of this report!; Methodology: measurement of inequality with the use of Gini.

Read the report in PDF here ...

Land: INT

LI publishes The prosperity index

ID: 201411192113

Is a nation’s prosperity defined solely by its GDP? Prosperity is more than just the accumulation of material wealth, it is also the joy of everyday life and the prospect of an even better life in the future. This is true for individuals as well as nations. The Prosperity Index is a global measurement of prosperity based on both income and wellbeing.

Find out more here

The econometric analysis of LI has identified 89 variables, which are spread across eight sub-indices:

1) Economy;

2) Governance;

3) Entrepreneurship & Opportunity;

4) Education;

5) Health;

6) Personal freedom;

7) Safety & Security;

8) Sociale Capital & Social Values.

Each of the 8 variables are subdivided in two: 1) having an effect on income 2) having an impact on wellbeing.

The sociological data were mainly retrieved from the Gallup World Poll.

Methodology for income and wellbeing scores. For each country, the latest data available in 2013 were gathered for the 89 variables. The raw values are standardised and multiplied by the weights. The weighted variable values are then summed to produce a country’s wellbeing and income score in each sub-index. The income and wellbeing scores are then standardised so that they can be compared.

Critical note LT: a) What we miss in the Prosperity Index is some kind of measurement of inequality and the measured effect of taxes on income redistribution (e.g. Gini before and after taxation). b) The GDP/capita is not critisized by Legatum Institute for being a variable not taking into account inequality.

Find out more here

The econometric analysis of LI has identified 89 variables, which are spread across eight sub-indices:

1) Economy;

2) Governance;

3) Entrepreneurship & Opportunity;

4) Education;

5) Health;

6) Personal freedom;

7) Safety & Security;

8) Sociale Capital & Social Values.

Each of the 8 variables are subdivided in two: 1) having an effect on income 2) having an impact on wellbeing.

The sociological data were mainly retrieved from the Gallup World Poll.

Methodology for income and wellbeing scores. For each country, the latest data available in 2013 were gathered for the 89 variables. The raw values are standardised and multiplied by the weights. The weighted variable values are then summed to produce a country’s wellbeing and income score in each sub-index. The income and wellbeing scores are then standardised so that they can be compared.

Critical note LT: a) What we miss in the Prosperity Index is some kind of measurement of inequality and the measured effect of taxes on income redistribution (e.g. Gini before and after taxation). b) The GDP/capita is not critisized by Legatum Institute for being a variable not taking into account inequality.

Land: INT

on taxes

ID: 201411171214

We must also make sure that big businesses pay their fair share of taxes. Ensuring these taxes are paid is vital in sustaining the low taxes at the heart of our plan, enabling hardworking families and businesses to keep more of the money they earn. We reached a G20-level agreement to ensure that there is nowhere for large companies to hide to avoid paying the taxes that are due. The G8 meeting I chaired in Northern Ireland also forged a ground-breaking initiative to stop the true owners of companies hiding behind a veil of secrecy, tackling the cancer of corruption that does so much to destroy countries and increase the risk to our own security. In Brisbane we also reached agreement to extend this work to cover the whole G20.

src: The Guardian 20141117

src: The Guardian 20141117

Land: GBR

Are the taxes paid now in Katanga?

ID: 201411120212

Democratic Republic of Congo is owed an estimated $3.7 billion in unpaid customs duties and fines by companies operating in its copper-rich Katanga province between 2008 and 2013, according to an unpublished report commissioned by the public prosecutor's office. (Reuters, 20140130) The report is disputed by the mine owners. Congo's budget is expected to be $8.2 billion in 2014.

Land: COD

Uniformisation des taxes

ID: 201411080130

L'ancienne ministre danoise, qui aura en charge d'examiner les révélations touchant les aides jugées trop généreuses accordées par le Luxembourg à certaines entreprises, a appelé à une uniformisation des taxes au sein de l'Europe. - Vestager wants tax uniformisation in Europe

(src: Nouvels Obs) - Good girl!

(src: Nouvels Obs) - Good girl!

Pepsi, IKEA, AIG, Coach, Deutsche Bank, Abbott Laboratories and nearly 340 other companies have secured secret deals from Luxembourg that allowed many of them to slash their global tax bills. PWC involved.

ID: 201411060126

see this link

The International Consortium of Investigative Journalists collaborated with more than 80 journalists in 26 countries in its Luxembourg Leaks investigation, exploring the secret tax deals global corporations have made with Luxembourg. For Belgium MO Magazine, De Tijd and Le Soir were involved in the investigation.PricewaterhouseCoopers has helped multinational companies obtain at least 548 tax rulings in Luxembourg from 2002 to 2010. These legal secret deals feature complex financial structures designed to create drastic tax reductions. The rulings provide written assurance that companies’ tax-saving plans will be viewed favorably by Luxembourg authorities.

The International Consortium of Investigative Journalists collaborated with more than 80 journalists in 26 countries in its Luxembourg Leaks investigation, exploring the secret tax deals global corporations have made with Luxembourg. For Belgium MO Magazine, De Tijd and Le Soir were involved in the investigation.PricewaterhouseCoopers has helped multinational companies obtain at least 548 tax rulings in Luxembourg from 2002 to 2010. These legal secret deals feature complex financial structures designed to create drastic tax reductions. The rulings provide written assurance that companies’ tax-saving plans will be viewed favorably by Luxembourg authorities.

Companies have channeled hundreds of billions of dollars through Luxembourg and saved billions of dollars in taxes. Some firms have enjoyed effective tax rates of less than 1 percent on the profits they’ve shuffled into Luxembourg.

Many of the tax deals exploited international tax mismatches that allowed companies to avoid taxes both in Luxembourg and elsewhere through the use of so-called hybrid loans.

In many cases Luxembourg subsidiaries handling hundreds of millions of dollars in business maintain little presence and conduct little economic activity in Luxembourg. One popular address – 5, rue Guillaume Kroll – is home to more than 1,600 companies.

The International Consortium of Investigative Journalists collaborated with more than 80 journalists in 26 countries in its Luxembourg Leaks investigation, exploring the secret tax deals global corporations have made with Luxembourg. For Belgium MO Magazine, De Tijd and Le Soir were involved in the investigation.PricewaterhouseCoopers has helped multinational companies obtain at least 548 tax rulings in Luxembourg from 2002 to 2010. These legal secret deals feature complex financial structures designed to create drastic tax reductions. The rulings provide written assurance that companies’ tax-saving plans will be viewed favorably by Luxembourg authorities. Companies have channeled hundreds of billions of dollars through Luxembourg and saved billions of dollars in taxes. Some firms have enjoyed effective tax rates of less than 1 percent on the profits they’ve shuffled into Luxembourg.

Many of the tax deals exploited international tax mismatches that allowed companies to avoid taxes both in Luxembourg and elsewhere through the use of so-called hybrid loans.

In many cases Luxembourg subsidiaries handling hundreds of millions of dollars in business maintain little presence and conduct little economic activity in Luxembourg. One popular address – 5, rue Guillaume Kroll – is home to more than 1,600 companies.

Verhuis maatschappelijke zetel naar 'tax heavens' al jaren aan de gang

ID: 201411042252

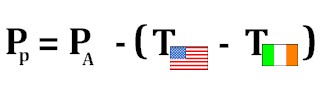

Bloomberg en andere Amerikaanse media rapporteren al jaren over het fenomeen dat grote - zelfs beursgenoteerde bedrijven - hun maatschappelijke zetel verhuizen naar belastingparadijzen. (zie U.S. Companies Beat the System With Irish Addresses) In het jargon van fiscale specialisten wordt zo'n operatie 'inversion' genoemd. Tien jaar geleden stemde het Congres van de US een 'anti-inversion'-wet om delocalisatie van maatschappelijke zetels en de daaraan verbonden belastingvlucht tegen te gaan. Die wet van 2004 (in feite een kanjer van een kaderwet die in sneltreinvaart onder de titel American Jobs Creation Act werd goedgekeurd) liet echter een serieus en niet onschuldig republikeins achterpoortje open: tijdens een 'merger' met een niet-Amerikaans bedrijf mogen de Amerikaanse bedrijven hun zetel naar elders verhuizen. In feite ondersteunde de USA op die manier rechtstreeks de jacht op (Europese) bedrijven: met de tax-reductie alleen al kon men een deel van (of geheel) de overname(-s) financieren. Dit laat zich uitdrukken in een formule (hier met een voorbeeld voor Ierland): Pp = PA - (Tusa - Teire) . Deze formule zegt niets anders dan: The price paid equals the price of the acquisition minus the difference between taxes in the USA and the taxes paid in Ireland. In sommige gevallen gaat het om miljarden dollars. Populaire bestemmingen van de verhuizers zijn Zwitserland, Bermuda, Ierland, UK.

Jacob J. Lew, de U.S. Treasury Secretary, deed op 27 juli 2014 in The Washington Post een dringende oproep om de wet van 2004 te wijzigen: Close the tax loophole on inversions. Een dringende oproep dat wel, maar de ondertoon is er een van machteloosheid. Het argument dat de gehele Amerikaanse infrastructuur (inclusief het formidabele defensiebudget) dreigt te kapseizen wanneer de gewone belastingbetaler (lees: de middenklasse) die alleen moet dragen, snijdt hout.

Anderzijds is het klaar dat de klassieke investeringstroeven zoals een hardwerkende en goed opgeleide bevolking, redelijke loonkosten, degelijk universitair onderwijs, goede wegen en havens, ondergeschikt geraken aan die ene vraag: wat is het taxpercentage in een land?

Vanuit Europees oogpunt is 'inversion' een bedreiging omdat - zoals gezegd - het taksvoordeel het wegkopen van Europese bedrijven faciliteert. Maar er is meer. Eens een multinational neerstrijkt in een EU-lidstaat en daar massaal de staatskas spijst, wordt die lidstaat als het ware een natuurlijke bondgenoot in Brussel om de op til zijnde merger niets in de weg te leggen. Wiens brood men eet, diens ... u weet wel. En omdat de concentratie van vermogens op een planetaire schaal gebeurt, is de democratische besluitvorming nationaal en internationaal in gevaar.

De verovering van de Senaat door de Republikeinen zal er geen goed aan doen.

Jacob J. Lew, de U.S. Treasury Secretary, deed op 27 juli 2014 in The Washington Post een dringende oproep om de wet van 2004 te wijzigen: Close the tax loophole on inversions. Een dringende oproep dat wel, maar de ondertoon is er een van machteloosheid. Het argument dat de gehele Amerikaanse infrastructuur (inclusief het formidabele defensiebudget) dreigt te kapseizen wanneer de gewone belastingbetaler (lees: de middenklasse) die alleen moet dragen, snijdt hout.

Anderzijds is het klaar dat de klassieke investeringstroeven zoals een hardwerkende en goed opgeleide bevolking, redelijke loonkosten, degelijk universitair onderwijs, goede wegen en havens, ondergeschikt geraken aan die ene vraag: wat is het taxpercentage in een land?

Vanuit Europees oogpunt is 'inversion' een bedreiging omdat - zoals gezegd - het taksvoordeel het wegkopen van Europese bedrijven faciliteert. Maar er is meer. Eens een multinational neerstrijkt in een EU-lidstaat en daar massaal de staatskas spijst, wordt die lidstaat als het ware een natuurlijke bondgenoot in Brussel om de op til zijnde merger niets in de weg te leggen. Wiens brood men eet, diens ... u weet wel. En omdat de concentratie van vermogens op een planetaire schaal gebeurt, is de democratische besluitvorming nationaal en internationaal in gevaar.

De verovering van de Senaat door de Republikeinen zal er geen goed aan doen.

Land: USA

Letter to Mme Judith Stelmach (ORF)

ID: 199810160928

ORF

Mme Judith Stelmach

Audience Research Department

Würzburggasse 30

A - 1136 - WIEN

Austria

Antwerp (Belgium), 1998-10-16

Dear Judith,

Please find hereby the Annual Report of the Flemish Licence Fee organisation (Dienst Kijk- en Luistergeld).

MERS is the external consultant for licence fee collection in Flanders, the Flemish speaking community of federalised Belgium.

On April 1st 1997 the service gained autonomy. Before that date the licence fee organisation was a part of Belgacom, the telecom operator of Belgium, privatised for some years now.

CIPAL, a service company in the informatic field and owned by a large number of cities in Flanders, took over the job (computer technology, organisation and management, etcetera). The Flemish government is the final responsable for and beneficiant of the tax collection. The public broadcast company (VRT) gets a dotation from the Flemish government but one can not say that there is an direct link between the taxes collected and the funding of the public broadcaster. This stays a political decision on a yearly basis. In some respect this situation makes the communication with the public rather difficult ("why you should pay licence fee"). Yet the collected licence fees are considered by the large majority as the main financial source for the VRT.

Note also that taxes are collected per household for TV-sets and per car for car radio.

As of April 1997 CIPAL undertook a number of successfull and speedy actions to improve the organisation of the service: new software, upgrading and training of personnel, large media campaign against tax evasion, etc.

All these efforts resulted in a dramatic rise of the registration rate in Flanders (see the tables in the annual report).

The situation in Flanders is somewhat special because of the very high penetration of cable (teledistribution). This makes it possible to match the databases of cable companies and the licence fee organisation on a nominative basis. This matching proces was made possible by law.

Great efforts go to the improvement of the matching methods because this is one of the keys for evasion rate reduction. The maps at the end of the annual report gives an insight in the evasion rate per province/city/village in Flanders (308 in total). The maps indicate where TV and car radio tax evasion is prominent and this information is to be considered as a management tool for specific and punctual action in the field.

It is my firm belief that international cooperation and data interchange can improve our business. Permanent improvement in tax collection can only evolve when brains work together and ideas flow around the globe.

Kind regards,

Lucas TESSENS

Managing Director MERS

Mme Judith Stelmach

Audience Research Department

Würzburggasse 30

A - 1136 - WIEN

Austria

Antwerp (Belgium), 1998-10-16

Dear Judith,

Please find hereby the Annual Report of the Flemish Licence Fee organisation (Dienst Kijk- en Luistergeld).

MERS is the external consultant for licence fee collection in Flanders, the Flemish speaking community of federalised Belgium.

On April 1st 1997 the service gained autonomy. Before that date the licence fee organisation was a part of Belgacom, the telecom operator of Belgium, privatised for some years now.

CIPAL, a service company in the informatic field and owned by a large number of cities in Flanders, took over the job (computer technology, organisation and management, etcetera). The Flemish government is the final responsable for and beneficiant of the tax collection. The public broadcast company (VRT) gets a dotation from the Flemish government but one can not say that there is an direct link between the taxes collected and the funding of the public broadcaster. This stays a political decision on a yearly basis. In some respect this situation makes the communication with the public rather difficult ("why you should pay licence fee"). Yet the collected licence fees are considered by the large majority as the main financial source for the VRT.

Note also that taxes are collected per household for TV-sets and per car for car radio.

As of April 1997 CIPAL undertook a number of successfull and speedy actions to improve the organisation of the service: new software, upgrading and training of personnel, large media campaign against tax evasion, etc.

All these efforts resulted in a dramatic rise of the registration rate in Flanders (see the tables in the annual report).

The situation in Flanders is somewhat special because of the very high penetration of cable (teledistribution). This makes it possible to match the databases of cable companies and the licence fee organisation on a nominative basis. This matching proces was made possible by law.

Great efforts go to the improvement of the matching methods because this is one of the keys for evasion rate reduction. The maps at the end of the annual report gives an insight in the evasion rate per province/city/village in Flanders (308 in total). The maps indicate where TV and car radio tax evasion is prominent and this information is to be considered as a management tool for specific and punctual action in the field.

It is my firm belief that international cooperation and data interchange can improve our business. Permanent improvement in tax collection can only evolve when brains work together and ideas flow around the globe.

Kind regards,

Lucas TESSENS

Managing Director MERS

The Idea Of Owning Land

An old notion forged by the sword

is quietly undergoing a profound transformation

ID: 198412210004

One of the articles in Living With The Land (IC#8)

Originally published in Winter 1984 on page 5

Copyright (c)1985, 1997 by Context Institute

HOWEVER NATURAL “owning” land may seem in our culture, in the long sweep of human existence, it is a fairly recent invention. Where did this notion come from? What does it really mean to “own” land? Why do we, in our culture, allow a person to draw lines in the dirt and then have almost complete control over what goes on inside those boundaries? What are the advantages, the disadvantages, and the alternatives? How might a humane and sustainable culture re-invent the “ownership” connection between people and the land?

These questions are unfamiliar (perhaps even uncomfortable) to much of our society, for our sense of “land ownership” is so deeply embedded in our fundamental cultural assumptions that we never stop to consider its implications or alternatives. Most people are at best only aware of two choices, two patterns, for land ownership – private ownership (which we associate with the industrial West) and state ownership (as in the Communist East).

Both of these patterns are full of problems and paradoxes. Private ownership enhances personal freedom (for those who are owners), but frequently leads to vast concentrations of wealth (even in the U.S., 75% of the privately held land is owned by 5% of the private landholders), and the effective denial of freedom and power to those without great wealth. State ownership muffles differences in wealth and some of the abuses of individualistic ownership, but replaces them with the often worse abuses of bureaucratic control.

Both systems treat the land as an inert resource to be exploited as fully as possible, often with little thought for the future or respect for the needs of non-human life. Both assume that land ownership goes with a kind of exclusive national sovereignty that is intimately connected to the logic of war.

In short, both systems seem to be leading us towards disaster, yet what other options are there?

The answer, fortunately, is that there are a number of promising alternatives. To understand them, however, we will need to begin by diving deeply into what ownership is and where it has come from.

THE HISTORICAL ROOTS

Beginnings Our feelings about ownership have very deep roots. Most animal life has a sense of territory – a place to be at home and to defend. Indeed, this territoriality seems to be associated with the oldest (reptilian) part the brain (see IN CONTEXT, #6) and forms a biological basis for our sense of property. It is closely associated with our sense of security and our instinctual “fight or flight” responses, all of which gives a powerful emotional dimension to our experience of ownership. Yet this biological basis does not determine the form that territoriality takes in different cultures.

Humans, like many of our primate cousins, engage in group (as well as individual) territoriality. Tribal groups saw themselves connected to particular territories – a place that was “theirs.” Yet their attitude towards the land was very different from ours. They frequently spoke of the land as their parent or as a sacred being, on whom they were dependent and to whom they owed loyalty and service. Among the aborigines of Australia, individuals would inherit a special relationship to sacred places, but rather than “ownership,” this relationship was more like being owned by the land. This sense of responsibility extended to ancestors and future generations as well. The Ashanti of Ghana say, “Land belongs to a vast family of whom many are dead, a few are living and a countless host are still unborn.”

For most of these tribal peoples, their sense of “land ownership” involved only the right to use and to exclude people of other tribes (but usually not members of their own). If there were any private rights, these were usually subject to review by the group and would cease if the land was no longer being used. The sale of land was either not even a possibility or not permitted. As for inheritance, every person had use rights simply by membership in the group, so a growing child would not have to wait until some other individual died (or pay a special fee) to gain full access to the land.

Early Agricultural Societies Farming made the human relationship to the land more concentrated. Tilling the land, making permanent settlements, etc., all meant a greater direct investment in a particular place. Yet this did not lead immediately to our present ideas of ownership. As best as is known, early farming communities continued to experience an intimate spiritual connection to the land, and they often held land in common under the control of a village council. This pattern has remained in many peasant communities throughout the world.

It was not so much farming directly, but the larger-than- tribal societies that could be based on farming that led to major changes in attitudes towards the land. Many of the first civilizations were centered around a supposedly godlike king, and it was a natural extension to go from the tribal idea that “the land belongs to the gods” to the idea that all of the kingdom belongs to the god-king. Since the god-king was supposed to personify the whole community, this was still a form of community ownership, but now personalized. Privileges of use and control of various types were distributed to the ruling elite on the basis of custom and politics.

As time went on, land took on a new meaning for these ruling elites. It became an abstraction, a source of power and wealth, a tool for other purposes. The name of the game became conquer, hold, and extract the maximum in tribute. Just as The Parable Of The Tribes (see IN CONTEXT, #7) would suggest, the human-human struggle for power gradually came to be the dominant factor shaping the human relationship to the land. This shift from seeing the land as a sacred mother to merely a commodity required deep changes throughout these cultures such as moving the gods and sacred beings into the sky where they could conveniently be as mobile as the ever changing boundaries of these empires.

The idea of private land ownership developed as a second step – partly in reaction to the power of the sovereign and partly in response to the opportunities of a larger-than- village economy. In the god-king societies, the privileges of the nobility were often easily withdrawn at the whim of the sovereign, and the importance of politics and raw power as the basis of ownership was rarely forgotten. To guard their power, the nobility frequently pushed for greater legal/customary recognition of their land rights. In the less centralized societies and in the occasional democracies and republics of this period, private ownership also developed in response to the breakdown of village cohesiveness. In either case, private property permitted the individual to be a “little king” of his/her own lands, imitating and competing against the claims of the state.